Metro Atlanta went from roughly 120,000 home transactions in 2021 to just over 65,000 single-family sales in 2024, a collapse of about 46% according to the Atlanta Regional Commission's housing trend analysis. That single number changes the frame. A key question isn't whether Atlanta is still “hot.” It's whether you're shopping in the part of Atlanta that cooled down, or the part that never really did.

That distinction matters more than the citywide median, more than the headlines, and often more than broad advice from national housing sites. Buyers who treat Atlanta as one market can misread both risk and opportunity. Some neighborhoods now offer real negotiating room. Others still punish hesitation.

If you're asking whether now is a good time to buy a home in Atlanta, the useful answer is conditional. For the right buyer, in the right submarket, yes. But the decision only makes sense when you separate metro trends from neighborhood realities and then match both to your finances.

Atlanta's 2026 Housing Market Temperature Check

Atlanta enters 2026 with a split personality. Across metro Atlanta, sales activity remains far below the pandemic peak, while prices have given back only a modest portion of their run-up. That combination matters because it creates two very different buyer experiences. In many intown neighborhoods, limited supply still keeps well-priced homes competitive. In many suburban pockets, slower turnover has given buyers more room to inspect, compare, and negotiate.

The key shift is activity, not headline pricing. As noted earlier, metro Atlanta transactions fell sharply from 2021 to 2024. Median prices, by contrast, held up much better and only pulled back modestly in early 2025. A market where transaction volume drops faster than prices signals friction rather than broad-based confidence. Buyers are still present. They are more payment-sensitive, more selective, and less willing to waive diligence to win a deal.

What the shift says about buyer behavior

The same metro trend data cited earlier also showed a smaller median home size sold in 2025, while the median construction year stayed relatively dated. That pattern suggests buyers are changing the type of home they will accept, not just waiting for a lower price on the same product.

In practical terms, affordability pressure is pushing households toward smaller homes, older homes, or locations farther from the urban core. That is one of the clearest signs that Atlanta is no longer moving as a single market. A buyer choosing between Virginia-Highland and western Gwinnett is not facing the same set of constraints, even if both searches appear under the same metro median price.

One sentence sums up the current temperature check. Atlanta has cooled unevenly.

That uneven cooling helps explain why broad statistics can feel disconnected from what buyers see on the ground. Intown areas with strong school zones, short commutes, and limited resale inventory can still behave like a seller's market. Outer suburban areas with more new construction, longer commute tradeoffs, or higher investor activity often give buyers more bargaining power. The useful question is not whether Atlanta is hot or cold. It is which Atlanta you are shopping in.

Why broad-market data only gets you halfway

Metro numbers help you set expectations, but they do not tell you how to bid on a specific block, subdivision, or school cluster. Buyers need neighborhood-level evidence. Tools such as real estate comps and lead gen platforms can help compare recent sales, listing age, and price reductions in the exact area you are targeting.

Atlanta's economic base still supports housing demand over the longer run, even with slower turnover today. Job growth, business relocation, and household formation continue to shape who needs housing and where that demand shows up. This overview of how Atlanta's economy is driving growth across Georgia provides useful context for why demand has softened without fully breaking.

For buyers, the takeaway is straightforward. The market is no longer uniformly overheated, but it is not uniformly soft either. If you can identify whether you are buying in the intown Atlanta that still rewards speed or the suburban Atlanta that increasingly rewards patience, your strategy gets much sharper.

Decoding Price Predictions and Market Risks

The most confusing part of today's Atlanta market is that several credible signals point in different directions at the same time.

A May 2025 Cotality report ranked Atlanta as the #2 highest-risk market in the U.S. among the largest metros for a significant home price decline, with a projected 10% to 15% correction from recent peaks, as summarized in this Atlanta housing risk report. That would be a meaningful adjustment for anyone buying with a short time horizon.

But even the pricing data used to discuss Atlanta's slowdown isn't fully aligned. The same report notes that Zillow showed a 2.4% year-over-year decline while Redfin showed a 10.6% drop, with Redfin putting the median sale price at $380,000 in February 2025.

Why the headlines feel contradictory

Different platforms measure slightly different slices of the market. They may weight listings, closed sales, housing types, or geography differently. For a buyer, that means one important thing. You shouldn't build your strategy around a single headline number.

The same risk summary also points to the Case-Shiller Home Price Index for Atlanta at 248.93, down 0.00% from one year earlier and up only 0.30% month over month in the cited analysis. That's not a market in full retreat. It's a market that has largely stopped climbing.

Buying into a plateau is different from buying into a boom. You gain less upside momentum, but you also avoid bidding in a market that's running away from you.

How to think about risk without freezing

For most buyers, the primary concern isn't that prices might soften a bit after closing. A greater risk is making a decision that assumes Atlanta is easy to predict.

A practical way to read today's signals:

- Short-term buyers face more exposure. If you may need to move again soon, a possible correction matters more.

- Long-term owner-occupants can absorb more volatility. A temporary paper loss matters less if the home fits your life for years.

- Neighborhood selection matters more than metro headlines. Some areas are already showing softer pricing while others remain defended by location and scarcity.

Commercial real estate often shows this kind of uneven repricing before residential buyers fully register it. That's one reason this analysis of the future of commercial real estate in Atlanta is useful background. It highlights how one metro can contain very different demand patterns at the same time.

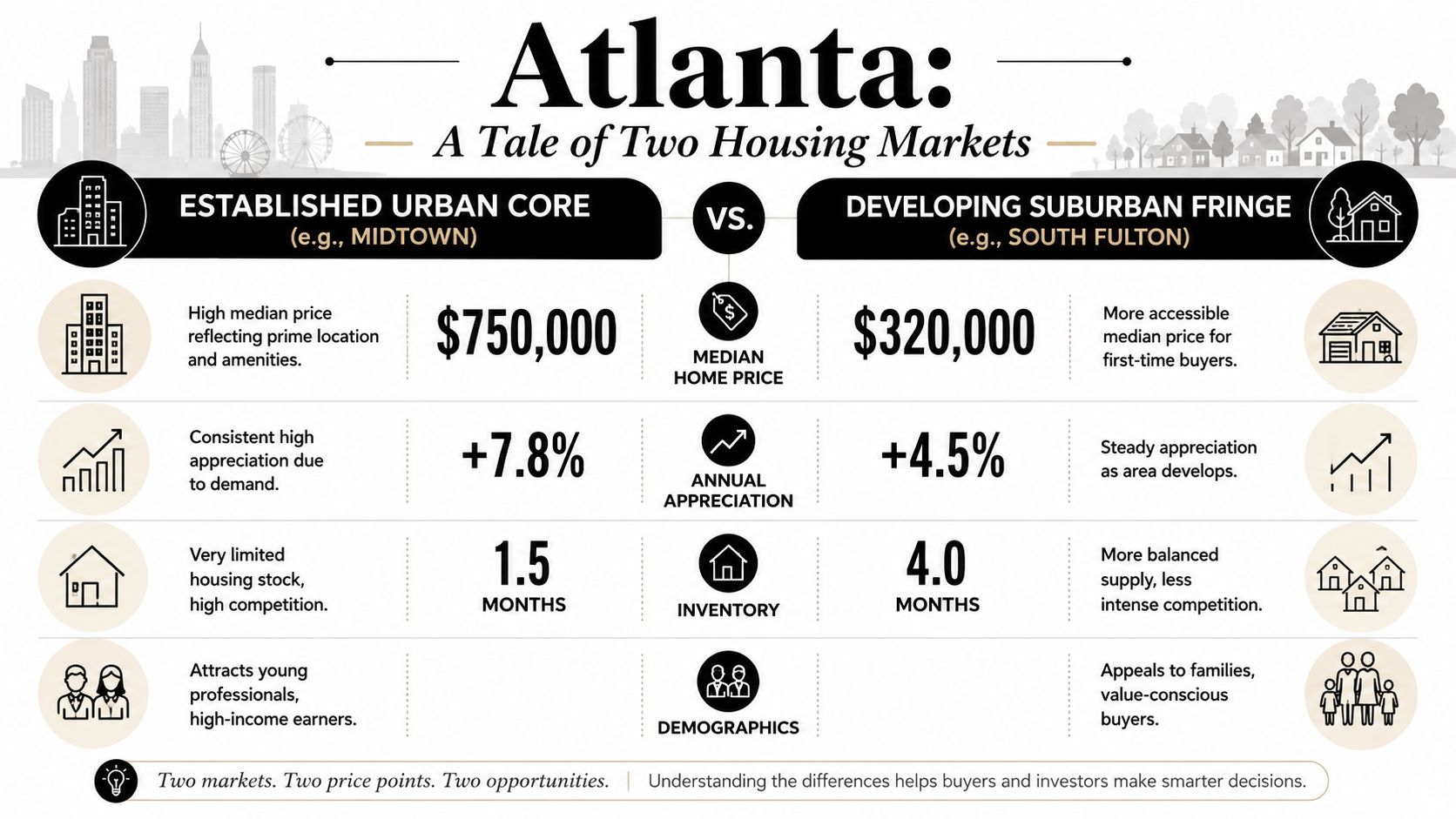

Why Your Neighborhood Defines Your Buying Power

Most articles on whether now is a good time to buy a home in Atlanta miss the core issue. There isn't one Atlanta market. There are at least two, and they behave differently enough that a citywide answer becomes misleading.

The strongest evidence is simple. 68% of homes sell below list price citywide, yet intown walkable neighborhoods such as Virginia-Highland and Candler Park still move with 7 to 14 day sales cycles, according to this Atlanta neighborhood market breakdown. In suburban areas such as Roswell, the same source notes that median pricing has already moved lower year over year.

That's the market bifurcation buyers need to understand.

The intown market still rewards speed

In neighborhoods where walkability, school access, historic charm, and commute convenience overlap, demand stays concentrated even when the broader metro cools. Buyers in those pockets often compete for a narrow set of homes that check the same boxes.

If that's your target, your negotiating power may be much weaker than citywide statistics suggest.

| Market type | What it often feels like for buyers | Best response |

|---|---|---|

| Intown walkable neighborhoods | Limited inventory, faster decisions, less room to push on price | Move quickly, know your ceiling, keep contingencies realistic |

| Softer suburban pockets | More options, longer decision windows, more willingness from sellers | Negotiate credits, repairs, and terms instead of fixating only on list price |

The suburban market offers a different kind of opportunity

In slower suburban submarkets, the power often isn't dramatic price cutting. It's better terms.

A seller might be more open to repair requests, closing-cost help, or flexibility around timing. Buyers who only focus on headline price can miss those gains. In a higher-rate environment, terms matter because they affect total cost and monthly cash flow, not just the sticker number.

Neighborhood test: If homes like the one you want still disappear in under two weeks, you're probably not in a buyer's market even if Atlanta overall looks softer.

How to identify which Atlanta you're shopping in

Ask these questions before making assumptions:

- How fast do comparable homes go pending? Speed tells you more than list-price rhetoric.

- Are reductions common before contract? Repeated cuts usually signal weak pricing power.

- Do similar homes return to market? Failed contracts can point to inspection issues or shaky demand.

- What are sellers conceding privately? Agent remarks and contract chatter often reveal more than the final sale price.

Buyers moving to intown neighborhoods should also understand the lifestyle premium they're paying for. This local guide to the Atlanta BeltLine for visitors and locals is a good reminder that access, mobility, and neighborhood identity shape demand in ways a metro median never can.

Aligning Your Finances with Current Market Realities

Even if the submarket looks favorable, the purchase only works if your numbers work.

That sounds obvious, but many buyers still start with what a lender might approve instead of what they can comfortably carry. Those are not the same figure. Approval capacity reflects lender standards. Real affordability reflects your life, your risk tolerance, and your other obligations.

Build your budget from monthly comfort, not maximum approval

Start with the full monthly housing cost you can carry without crowding out savings, repairs, or normal living expenses. Then work backward.

Include more than principal and interest. A realistic budget should account for property taxes, homeowners insurance, utilities, routine maintenance, and the cash drain that follows any move. Older homes especially can require immediate spending after closing, even when they pass inspection.

A house payment that looks manageable on paper can still feel expensive if it leaves you with no flexibility the first time something breaks.

Stress-test your own profile

Use a simple self-audit before you shop seriously:

- Income stability matters first. If your job situation is changing, timing risk may outweigh market opportunity.

- Debt load changes your comfort level. Credit cards, car loans, student debt, and childcare all reduce practical buying power.

- Cash reserves matter after closing. You don't want every available dollar tied up in the purchase.

- Credit quality affects options. Stronger credit usually means better financing choices and a smoother approval path.

A smart buyer also separates wants from essential needs. Commute, schools, home office space, and renovation tolerance all affect what you can safely buy. The more compromise a household can handle, the more room it has to adapt to current pricing.

Atlanta's broader business trajectory also shapes household confidence and relocation patterns over time. This overview of Atlanta business trends that will shape the next decade is useful context if you're buying with a long employment horizon in mind.

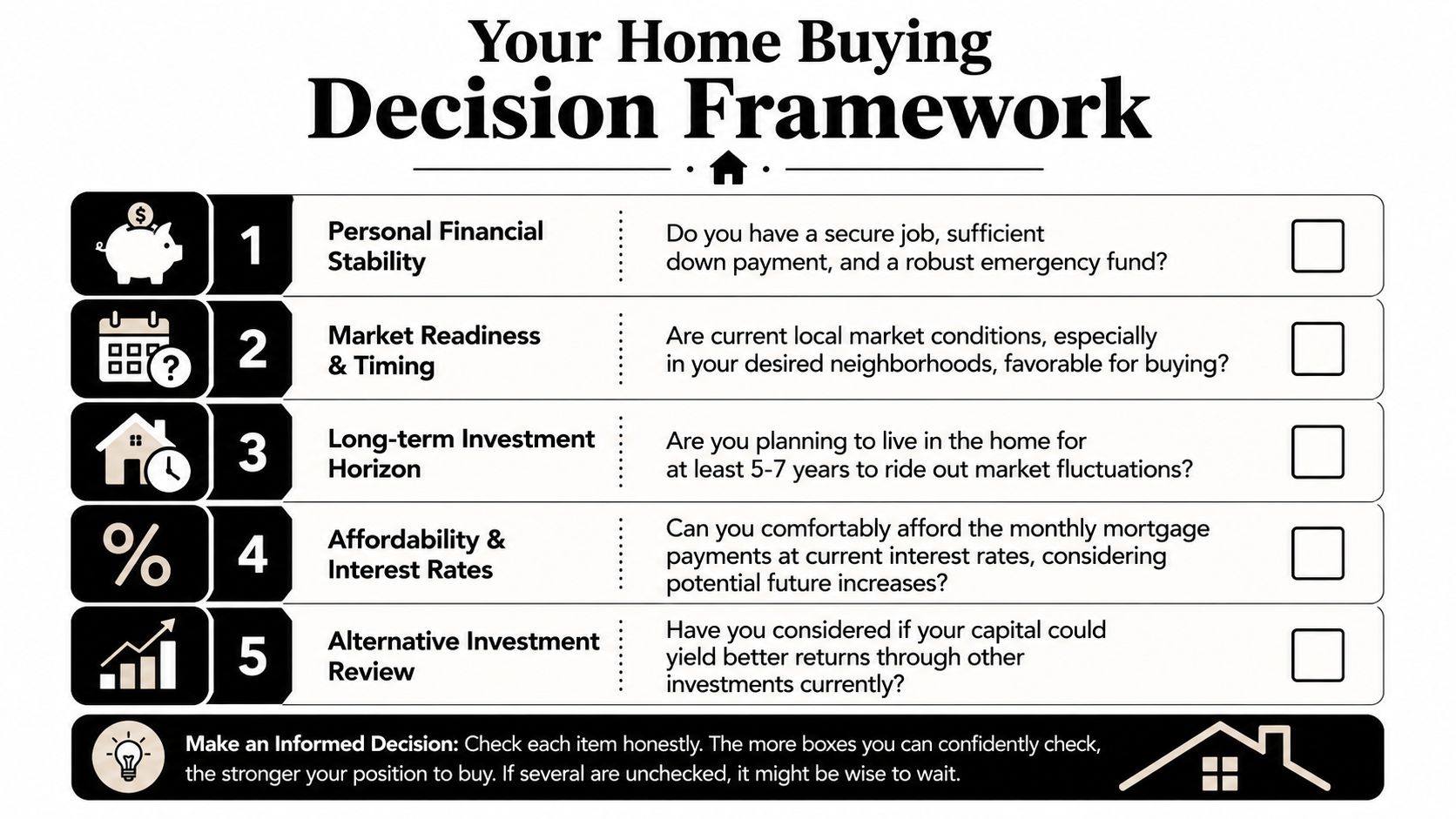

A Decision Framework for Buying Versus Waiting

The right time to buy isn't a calendar answer. It's the point where market conditions, personal finances, and life timing line up well enough that waiting no longer improves your odds.

That means you need a framework, not a hot take.

Three questions matter more than the headline answer

Is your target neighborhood favorable enough right now

If you're buying in a soft suburban pocket, waiting may not produce a dramatically better entry point than the concessions available today. If you're chasing a tightly held intown neighborhood, waiting may only mean competing again later for the same kind of scarce inventory.

Are your finances ready for ownership, not just purchase

A buyer can be ready to close and still not be ready to own. The difference shows up after move-in, when maintenance, furnishing, commuting changes, and normal life expenses continue.

Does your timeline absorb market noise

The shorter your ownership horizon, the more price volatility matters. The longer your horizon, the more your decision should center on fit, affordability, and neighborhood quality.

A practical self-check

Use this quick test:

- Buy now if you've identified a submarket where terms are workable, your monthly payment is comfortable, and you expect to stay put long enough to ride through normal fluctuations.

- Wait if your job situation is uncertain, your cash reserves are thin, or you're only buying because you fear being “priced out” later.

- Pause and refine if you like Atlanta broadly but haven't narrowed your search to a specific micro-market. That usually means you're still too early.

Decision lens: The best buyers don't ask whether Atlanta is good. They ask whether their exact purchase is good.

A long-term perspective helps here. Atlanta's role as an employment and innovation center still matters to future housing demand, which is why this look at Atlanta's growth as a Southeast tech hub is relevant context for buyers thinking beyond the next few quarters.

Making Your Move A Guide to Financing and Negotiation

Once you decide to move forward, execution matters as much as timing.

Start with a real pre-approval, not a casual pre-qualification. A strong pre-approval tells sellers your finances have already been vetted in a meaningful way. In competitive neighborhoods, that can matter almost as much as price. In slower areas, it gives you credibility while you negotiate terms.

Two different offer strategies for two different Atlantas

If you're buying in a high-competition intown pocket, focus on clarity and clean structure. Offer on the homes you want, know your walk-away number, and avoid negotiating over minor items that weaken your position early.

If you're buying in a softer suburban area, think beyond headline price. You may gain more by asking for closing-cost help, repair credits, flexible closing timing, or a rate-related concession than by forcing a small reduction that doesn't change your monthly payment much.

Inspections are more valuable in a calmer market

A slower market gives buyers room to investigate condition instead of waiving concerns out of fear. Use that room.

Pay close attention to roof age, HVAC performance, drainage, foundation issues, windows, and deferred maintenance. Older Atlanta housing stock can be appealing, but charm doesn't reduce replacement costs. Your inspection period isn't just about walking away from a bad house. It's about pricing the actual cost of ownership before you commit.

For buyers thinking long term, renovation judgment matters too. This guide on maximizing forever home value is a useful read because it shifts attention from cosmetic spending to improvements that support livability and resale over time.

The best negotiation strategy is the one that matches the market you are in. That's the central lesson. Don't bring an aggressive buyer's-market script into Virginia-Highland. Don't bring a bidding-war mindset into a suburban pocket where sellers are already blinking.

If your organization also needs secure, compliant disposition for retired IT equipment during a move, expansion, or office transition, contact Beyond Surplus for certified electronics recycling and secure IT asset disposal.