Metro Atlanta didn't just grow into a major data center market. It became the world's second-largest market behind Northern Virginia, while the amount of space under construction has been roughly doubling every six months since mid-2023, according to GovTech's reporting on Atlanta's market rise. That changes how IT leaders should think about Georgia. Atlanta is no longer a secondary option for overflow capacity. It's a serious platform for cloud, colocation, AI infrastructure, and the downstream operational work that follows every deployment.

For enterprise teams, the question isn't just why Atlanta is growing. It's why Atlanta keeps winning site-selection decisions even as the market gets more crowded, more power-hungry, and more operationally complex. The answer sits at the intersection of economics, connectivity, policy, and lifecycle planning.

Atlanta's Meteoric Rise in the Data Center World

Atlanta's ascent matters because scale changes behavior. Once a market reaches global relevance, carriers expand, construction ecosystems deepen, and enterprise buyers start treating the region as a strategic hub instead of a regional fallback.

Why the shift happened so fast

Atlanta moved from an emerging market to a hyperscale destination because several conditions lined up at once.

- Economics lined up early. Operators found a market that could support large campuses without the same cost profile seen in more saturated hubs.

- Infrastructure was already useful. Atlanta had the backbone needed to support enterprise and cloud traffic patterns, so builders didn't have to start from scratch.

- Policy signaled intent. State and local leaders treated data center development as a long-term economic strategy, not a one-off land deal.

That combination is why the phrase Why Atlanta Is a Prime Data Center Hub now has a practical answer, not just a marketing one. If you want a sense of how local infrastructure concentration is reshaping the region, this overview of top data centers in Atlanta and their impact is useful context.

Practical rule: Once a market becomes a top-tier hub, waiting too long to build local operating relationships usually costs more than entering early.

What decision-makers should take from it

For CIOs, infrastructure directors, and colocation buyers, Atlanta deserves the same level of diligence once reserved for older flagship markets. You're not evaluating a promising metro anymore. You're evaluating a market with enough gravitational pull to influence supplier availability, interconnection options, and future exit planning.

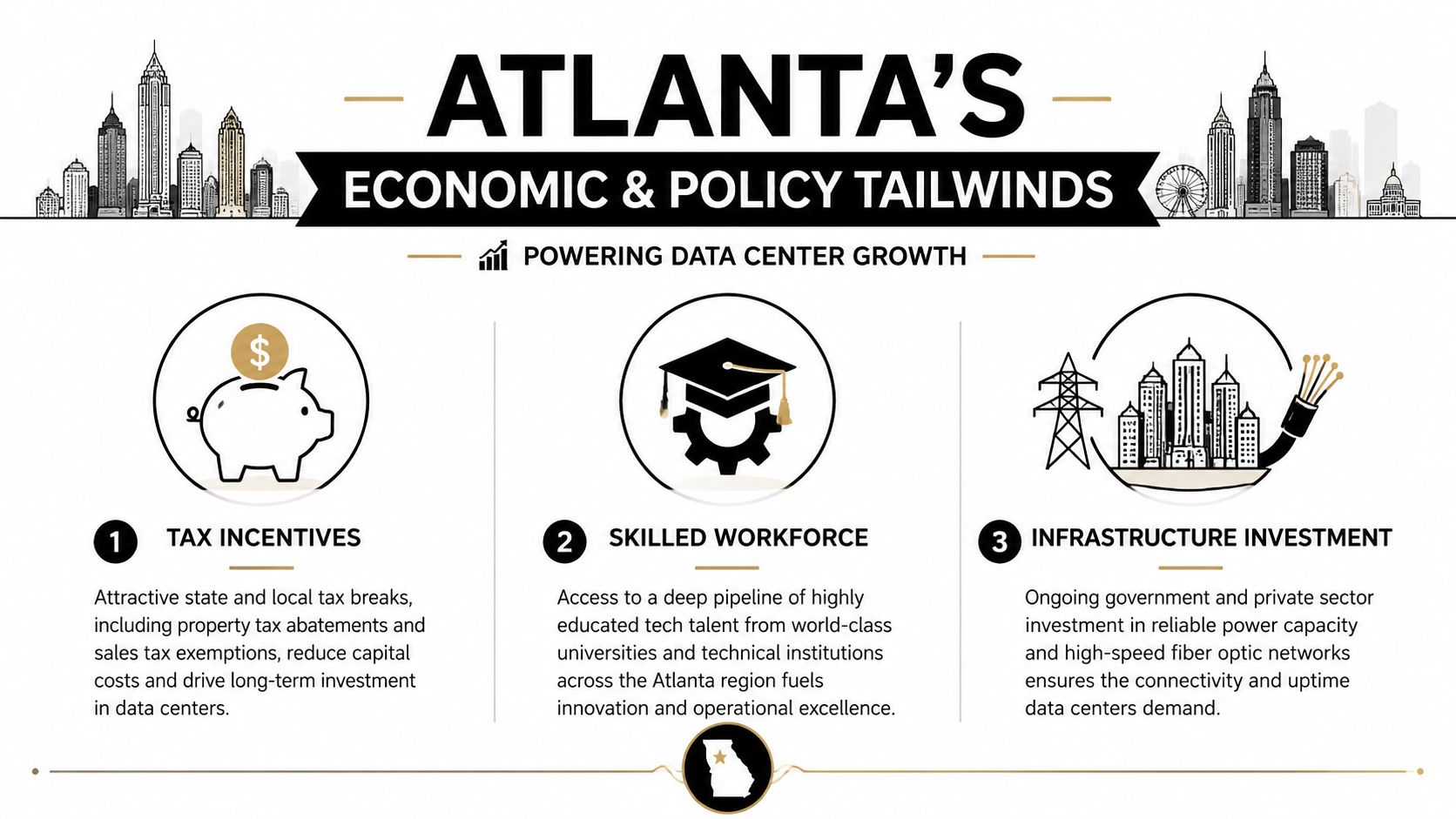

The Economic Engine Fueling Hyperscale Growth

Atlanta's growth story isn't accidental. It's backed by a cost structure and policy environment that large operators can model.

The economics operators actually care about

Georgia Trend points to several structural advantages that keep Atlanta in play for large-scale deployments: a healthy, reliable transmission grid, a regulated utility in Georgia Power, and a relatively low cost of doing business. Those are not abstract benefits. They affect financing assumptions, deployment schedules, and long-term operating risk.

The policy side is just as direct. Georgia's statewide data center incentive is projected to waive roughly $296 million in sales tax revenue in one year, while local governments have approved hundreds of millions of dollars in property tax savings to attract projects, as reported by Georgia Trend's analysis of Georgia data center dominance.

What works and what does not

A few patterns tend to separate workable Atlanta projects from weak ones.

| Decision area | What works | What does not |

|---|---|---|

| Power planning | Early utility coordination and realistic load assumptions | Treating power as a late-stage procurement item |

| Incentive strategy | Understanding state and local layers together | Looking only at headline tax relief |

| Financial modeling | Including construction, operations, and eventual retirement costs | Underwriting only for initial deployment |

Tax incentives help, but they don't rescue a bad site, a weak interconnection path, or poor lifecycle planning.

The business implication

Atlanta appeals to hyperscale and AI workloads because those workloads need stable operating conditions and room to scale. A market with workable power, a competitive cost base, and public incentives gives operators a cleaner path from approval to production.

Unpacking Atlanta's Strategic Connectivity and Infrastructure

Not every successful data center market wins on tax policy alone. Atlanta also works because it sits in the right place on the map and inside the right operating environment.

Connectivity that supports real workloads

STACK Infrastructure notes that Atlanta provides prime connectivity to major U.S. markets in both the Midwest and East Coast. For enterprise and cloud teams, that means Atlanta can support broad regional traffic patterns without forcing every workload into a coastal core.

That matters in practice when teams are balancing application performance, carrier diversity, and disaster recovery design. A market that can serve east-of-Mississippi demand efficiently gives architects more flexibility in how they place compute, storage, and replication.

Teams working through physical network expansion often pair data hall planning with broader transport and cabling decisions. In that context, local support for fiber optic installation near Atlanta becomes part of the site-readiness conversation, not a separate afterthought.

Policy shapes facility design

Georgia Tech's EPIcenter highlights another less-discussed advantage. State policy pushes new data centers toward closed-loop cooling and restricts open evaporative cooling towers unless an infeasibility exemption is granted, as outlined in Georgia Tech EPIcenter's data center policy overview.

That's more than a sustainability talking point. It changes engineering assumptions:

- Water planning gets stricter because operators have to think through long-term resilience earlier.

- Permitting becomes more design-sensitive because cooling choices aren't neutral.

- Operational predictability improves when facilities are built around water-risk constraints from the start.

A lot of markets can offer land. Fewer can offer the combination of backbone reach and a policy framework that pushes operators toward more durable infrastructure choices.

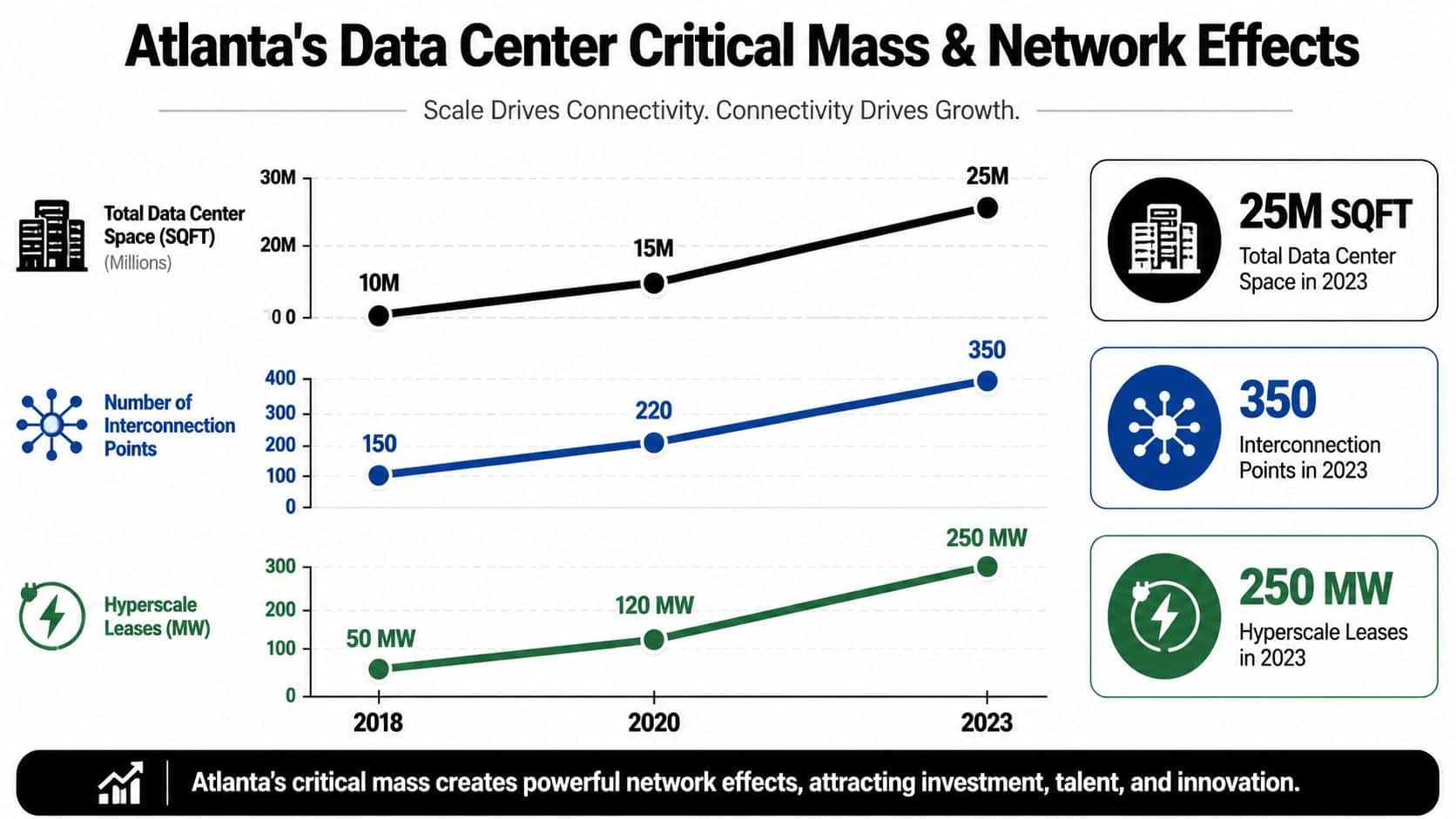

A Market Reaching Critical Mass and Network Effects

A market becomes self-reinforcing when demand, power, and ecosystem depth start feeding one another. Atlanta is at that stage.

The numbers that signal critical mass

As of early 2026, Atlanta's data center vacancy rate fell to 2% while the development pipeline reached 2.1 GW. CBRE also noted more than 3 GW of long-term power commitments, showing that operators are planning for sustained expansion tied to hyperscale and AI demand, according to CBRE's Atlanta data center market update.

Low vacancy by itself tells you supply is tight. The larger lesson is what happens next. Carriers, contractors, switchgear suppliers, commissioning firms, and decommissioning partners all start prioritizing a market that can keep producing deals.

Why this matters to operators and buyers

The benefit of critical mass is choice. In a denser market, buyers usually get:

- More ecosystem depth through colocated providers, carriers, and specialized service firms

- Better operational flexibility when expansion, migration, or consolidation plans change

- Stronger procurement advantage because more vendors want to stay active in the market

For a closer look at how this momentum is reshaping local infrastructure decisions, see Atlanta's data center boom and what to know.

In practical terms, a mature hub reduces the odds that one delayed vendor or one constrained provider derails the whole deployment plan.

Navigating Operational Risks and Sustainability Pressures

The bullish case for Atlanta is real. So are the constraints.

Growth doesn't remove friction

Data centers operate 24-7, and the Atlanta Regional Commission warns that fast expansion can pressure local resources if governments and operators don't define water and energy expectations early. The commission also highlights the need to consider closed-loop cooling, plan for droughts and outages, and manage stormwater, fire safety, lighting, and noise, as described in the Atlanta Regional Commission's guidance on data centers.

That's the part many growth stories skip. Demand can be strong while execution still gets harder. A market can be attractive and constrained at the same time.

The trade-offs operators need to face

Experienced teams usually test Atlanta projects against a tougher checklist than simple cost-per-megawatt assumptions.

- Interconnection risk can become a significant bottleneck even when land is available.

- Community acceptance matters more as facilities expand closer to mixed-use and suburban areas.

- Cooling and water decisions now affect permitting, resilience planning, and neighborhood scrutiny.

A site may look perfect in a spreadsheet and still become difficult if local expectations weren't addressed early. That's especially true for campuses with long build schedules and large backup power footprints.

What responsible operators do differently

The better approach is disciplined front-end planning.

| Pressure point | Better response |

|---|---|

| Water expectations | Define cooling strategy and utility coordination early |

| Neighborhood concerns | Address lighting, noise, traffic, and safety before hearings become adversarial |

| Utility dependence | Model phased growth instead of assuming immediate full buildout |

A workable Atlanta project isn't just one that secures land. It's one that can keep community support, utility alignment, and operating resilience over time.

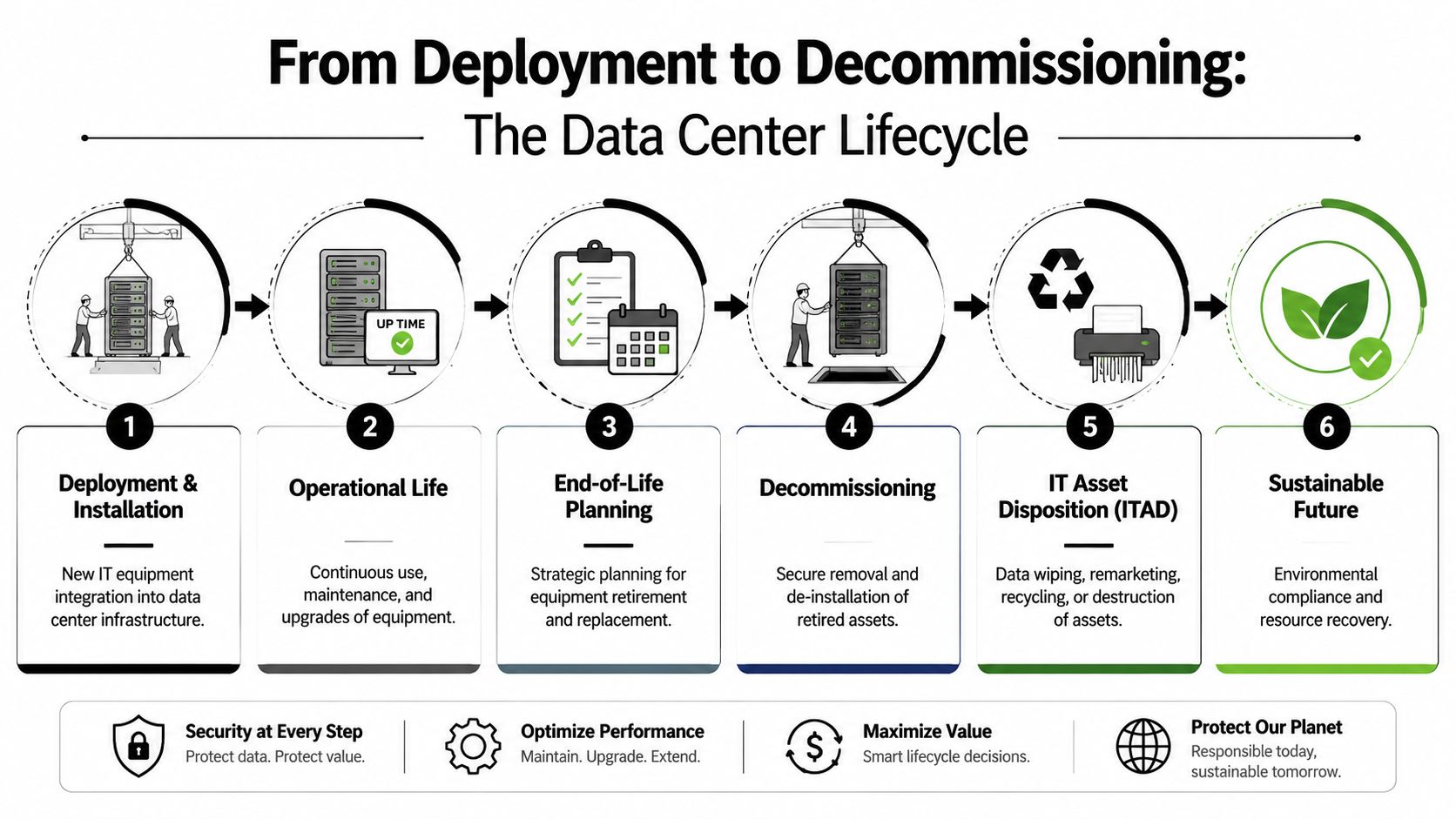

The Full Lifecycle Planning for Decommissioning and ITAD

Every rack installed in Atlanta starts a second clock. One measures useful life. The other measures how much risk and disposal cost will accumulate if retirement planning starts too late.

Why decommissioning belongs in the original plan

Teams usually give serious attention to redundancy, cooling, security, and commissioning. End-of-life planning often gets pushed to procurement closeout or facilities operations after the environment is already live. That delay creates avoidable exposure.

The problem is practical, not theoretical. A refresh or site exit can put retired servers, storage, switches, PDUs, batteries, and loose drives into the same loading paths used by active operations. If asset records are incomplete, chain of custody is weak, or data-bearing devices are mixed with scrap, the issue shifts from an operations task to a legal, compliance, and audit problem.

A disciplined plan covers four things from the start:

- De-installation sequencing that protects nearby production equipment

- Chain of custody controls for drives, tapes, and other media leaving the site

- Data destruction methods matched to policy, device type, and regulatory requirements

- Disposition routing that separates resale, redeployment, recycling, and destruction

That work should be built into the lifecycle budget, not treated as an afterthought.

What works in real projects

The best decommissioning projects are easier because the operating team made them easier months or years earlier. Asset tags are consistent. Rack positions are documented. Ownership is clear. Retirement triggers are defined before the first removal request lands.

In practice, the sequence matters as much as the vendor.

- Inventory the environment so retired assets are identified correctly before removal begins.

- Isolate data-bearing devices early, since they carry the highest compliance exposure.

- Sort reusable assets from scrap before staging and transport.

- Coordinate dock access, freight timing, and onsite escorts with facility operations.

- Record final disposition with audit-ready documentation, including destruction and recycling records where required.

For operators preparing for refresh cycles, consolidations, or full exits, these data center decommissioning trends in Atlanta show where projects tend to stall and what planning steps reduce that friction.

Where ITAD fits

IT asset disposition is part of infrastructure governance. It affects security, audit readiness, residual value recovery, and how fast a site can be cleared for reuse, retrofit, or lease turnover.

A provider like Beyond Surplus handles data center de-installations, logistics coordination, data wiping, hard drive shredding, IT buyback, and recycling documentation for business clients. That scope matters when enterprise teams need one process that covers physical removal, chain of custody, and downstream reporting without creating extra handoffs.

The right time to set the decommissioning process is while the equipment is still productive and fully documented.

Partnering for Success in the Atlanta Data Center Ecosystem

Atlanta has become a prime data center hub because it combines market scale, favorable economics, strategic connectivity, and policy support in a way few metros can match. That's the headline.

The more useful takeaway is operational. Winning in Atlanta takes more than securing capacity. Teams also need to evaluate power timing, cooling design, permitting friction, neighborhood impact, and the downstream burden of retiring infrastructure responsibly.

That full-lifecycle view is what separates a smart deployment from a costly one. The same market conditions that make Atlanta attractive for buildout also make disciplined exit planning more important. Hardware refreshes will accelerate. Consolidations will happen. Facilities will be retrofitted, rightsized, or vacated. When that starts, documentation, secure handling, and compliant disposition matter just as much as the original lease or construction agreement.

If your team is comparing providers, this guide on how to choose an ITAD vendor in Georgia step by step is a practical place to start.

If you're planning a refresh, migration, shutdown, or full facility cleanout in Atlanta, contact Beyond Surplus for certified electronics recycling and secure IT asset disposal.